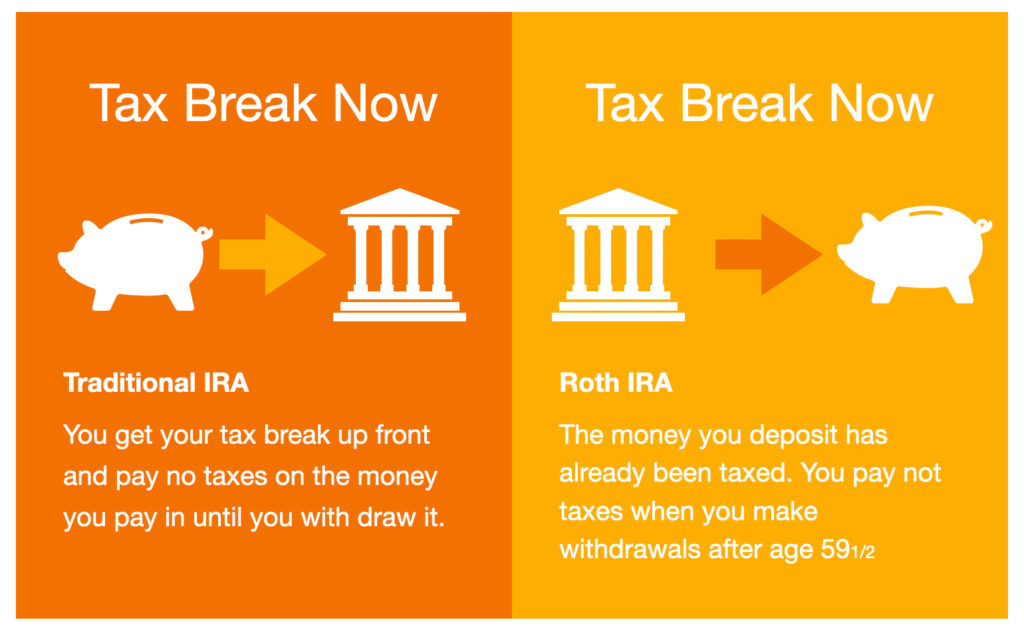

Four Questions on the Roth Five-Year Rule

The Roth “five-year rule” typically refers to when you can take tax-free distributions of earnings from your Roth IRA, Roth 401(k), or other work-based Roth account. The rule states that you must wait five years after making your first contribution, and the distribution must take place after age 59½, when you become disabled, or when […]

Four Questions on the Roth Five-Year Rule Read More »