This is the first of a two-part article on Dynamic versus Static Risk Strategy.

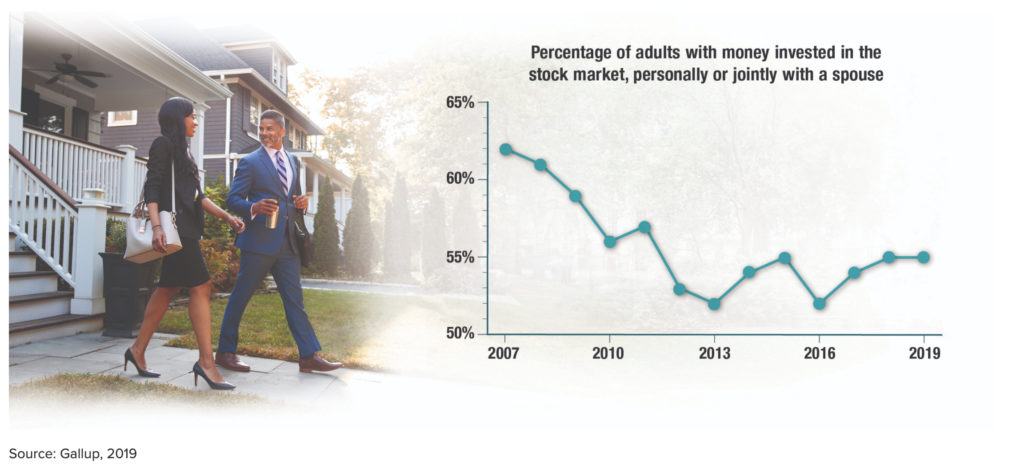

Fifty-five percent of Americans said that they (and/or a spouse) had money invested in the stock market in 2019. Since this is the same percentage of Americans as was reported in 2018, it’s obvious stock ownership still has a way to go before it recovers to pre-recession ownership levels. Cleary, stock market investor caution remains high despite a decade of strong market recovery.

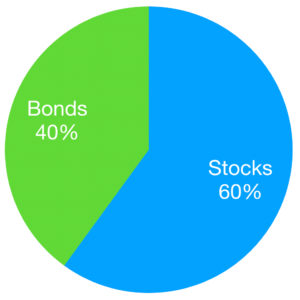

Where are people placing their investment bets? Most likely, they’re using a financial industry-standard method of managing portfolio risk, exemplified by the widely-used “60/40 portfolio.

A 60/40 portfolio refers to allocating 60% of asset investments to stocks and 40% to bonds. The “risk management” aspect of this strategy is the 40% of assets held in bonds, which are expected to act as a buffer to stocks during Bear markets. Bonds tend to hold up in times of stock distress.

The 60/40 portfolio is so common that investors can find a Balanced Fund by throwing a dart at the mutual funds page of their Sunday newspapers. This passive, unchanging method to manage risk is termed static risk management and it’s not the best approach.

We recommend a dynamic versus a static portfolio strategy. Why is that you ask?

If you think about it, a STATIC portfolio – with its constant, unchanging allocations to stocks and bonds – is a bit like preparing for any weather you might encounter by dressing half your body for warm weather and the other half for cold weather. On average, you’ll be comfortable. But, as that analogy shows, an average like that doesn’t really make much sense.

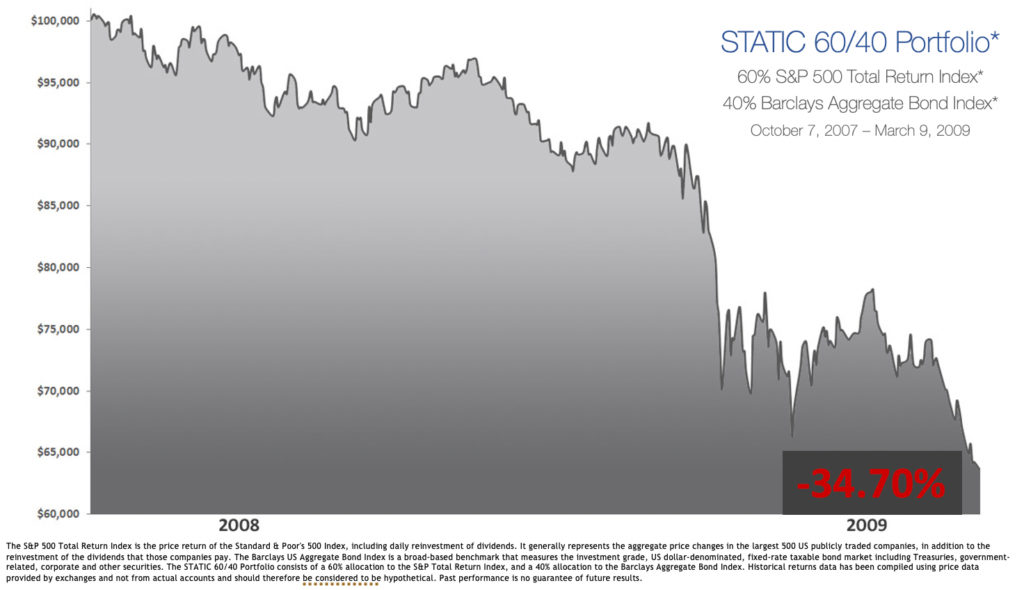

For example, if for the 2008 and 2009 bear market, we had a static risk-managed balanced portfolio of 60% stocks and 40% bonds, we’d have a top-to-bottom loss of -34.70%.

This loss is well beyond the risk tolerance capacity of the vast majority of investors and would be deemed a disaster by any reasonable person.

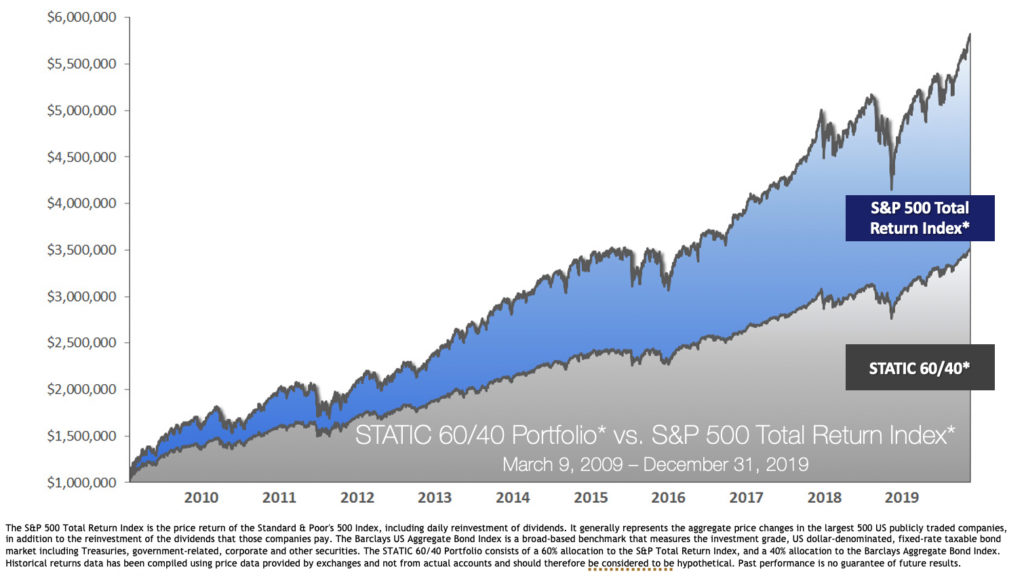

Now, consider what would happen with a static risk management approach in the subsequent up years that followed the recession. The 60/40 allocation wouldn’t have performed as well as it could have because of the drag on performance caused by the 40% bond allocation.

As you can see, STATIC risk management would have supplied too little protection in the recession, but too much to keep you from capitalizing on significant gains during the good times that followed.

The goal of Dynamic Risk Management is to apply more risk management in the bad times – when the need is greatest – and less in the good times – when the need is reduced.

In the second part installment of this article, we’ll cover how can you accurately identify the conditions in which more or less risk management should be applied.