This is the Third in a Four-part Series on Common Retirement Planning Mistakes

As I continue to mention in each part of this series (part 1 here and part 2 here), every year thousands of people still retire or attempt to retire without seeking professional advice or having a well-developed game plan for their retirement. Effective retirement planning should include coordinating the five primary planning areas of tax, healthcare (insurance), estate (legacy), investment and income. This can help to ensure you’re on the right track to meet your goals.

High Level – The Question of Fiduciary Best-Interest

In our industry, this is the big debate right now. Should all financial professionals be held to the same standard of care with their clients? Additionally, and more specifically to you, the debate is whether a financial advisor should put their clients’ interest before their own.

Stop and think about that for a moment. Why would you work with anyone who is not required to put your interest before their own? Implied in this question is the fact all financial professionals don’t have the same standard of care with you and your money. Sadly, that is correct.

Investment advisor representatives of Registered Investment Advisory firms are held to what is known as a “fiduciary standard” while registered representatives of Broker/Dealers are held to a “best-interest standard.” In general, and without going into great detail for the sake of space here, let’s look at these standards and how they apply to the professionals that you may consider handling your investments and retirement planning.

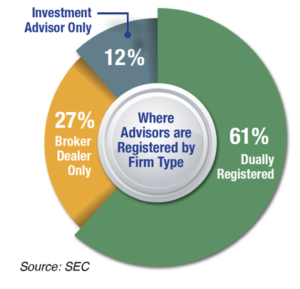

There are three types of classifications used for financial professionals:

- Fiduciary (Registered as an Investment Advisor Representative of a Registered Investment Advisory Firm)

- Non-Fiduciary (Registered as a Registered Representative of a Broker/Dealer)

- Hybrid (A combination of one and two)

So, what’s the difference between these three and what does it mean to you? It’s important to understand the terms.

Fiduciary

A fiduciary firm (Registered Investment Advisor) has a legal and ethical obligation to do what is in the best interest of the client. This means they put the client’s interest above those of the firm. Fiduciaries typically receive compensation in the form of fees regardless of the type of investments or activities they recommend for their clients. These fees are usually based on the number of assets they are managing or may be a flat fee negotiated in advance.

A fiduciary is required to put your interests first in building a financial plan and/or managing financial assets under a duty of good faith, care and trust. This is better known as the “prudent person standard of care.” This can be confusing so here’s a brief example of this standard of care. It could include removing or disclosing any conflicts of interest the fiduciary may have (such as compensation on the sale of a financial product) and disclosing what fees and expenses are present and how they may affect you. Representatives working for a Registered Investment Advisor are commonly called investment advisor representatives.

Non-Fiduciary

As of June 2019, the Securities and Exchange Commission (“SEC”) issued rules that non-fiduciary, Broker-Dealer firms are to meet a best-interest standard of conduct but it falls short of the fiduciary standard Registered Investment Advisor firms must meet. Generally, this allows them to make recommendations consistent with the needs and preferences of the customer at the time of the recommendation without being held to the fiduciary investment advice standard.

The non-fiduciary must reasonably believe a recommendation is suitable to a client’s objectives, needs and circumstances at the time of the investment, which is basically the same standard they were held to previously. Non-fiduciary’s are typically compensated through commissions on securities transactions but may also charge fees to access some parts of their platforms. Some do financial planning while others don’t.

Brokers (although commonly called by many different titles) are the representatives for broker-dealers. Although the June 2019 best-interest rule for non-fiduciaries was passed by the SEC, two other similar rules before it have been vacated. Currently, these types of firms are vehemently fighting against being held to the same fiduciary standard as investment advisors. It doesn’t take a big stretch of the imagination for you to understand why they are against being held to the fiduciary standard.

Hybrids or “dually-registered”

A hybrid structure normally has representatives who are registered both with a broker-dealer and an investment advisor. This means they have a fiduciary side and a non-fiduciary side regarding what they can offer clients. This approach can be fraught with danger and confusion for clients, who must determine if they are being given fiduciary advice or being sold a product.

Additionally, many financial industry regulators are asking these firms to explain how and why they chose to be a fiduciary for some clients (or transactions) and a non-fiduciary for others. It appears that even having to make that choice leaves a lot of room for questions as to intent. As a client, you should not have to wonder whether your adviser is a fiduciary or not. The critical questions to ask any potential financial advisor is this: What type of standards are they operating under when they are advising you? As a fiduciary, with your legal best interest in mind or not? It is a very fine line.

Things to consider:

- All three firm types can provide a valuable service. Everyone’s needs and desires are different and there can be good and bad in any model. That is free-market competition and you get to decide what’s right for you.

- Request full disclosure of all information from your financial professional to make the decision that you believe is right for you. Anything less, walk away.

- Do your homework. Ask a lot of questions. Call your state regulator or check out the representative’s background on brokercheck.finra.org. A professional should encourage and welcome this and be willing to answer whatever questions you may have.

- Look for someone with experience and professional credibility (designations), whom you connect with personally and who you believe you can trust to go the extra mile.

- Call or come visit us. As an independent, fee-based, fiduciary firm we are happy to answer whatever questions you may have and help further clarify what type of professional might be right for you and your retirement goals so you can make an informed choice.

If you don’t currently have a retirement advisor, we’d be delighted to schedule an introductory meeting with you to learn more about your current situation and your retirement goals. Contact us today to schedule an appointment!

Investment Advisory services offered through Game Plan Advisors, Inc., a registered investment advisor. Insurance services offered through Wootton Financial Group, Inc. Game Plan Advisors, Inc. and Wootton Financial Group, Inc. are affiliated through common ownership. Neither Game Plan Advisors, Inc nor Wootton Financial Group, Inc. offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.